Cryptocurrency mining has become a cornerstone of the blockchain ecosystem, powering decentralized networks and enabling the creation of new digital assets. In 2025, as the cryptocurrency market continues to mature, mining remains a lucrative yet complex activity, particularly in the United States. However, with its profitability comes significant tax obligations that miners must navigate.

The Internal Revenue Service (IRS) has been increasingly vigilant in enforcing tax compliance in the crypto space. According to Chainalysis, the global crypto adoption index grew by over 880% by 2021, with the U.S. ranking among the top countries for mining activity. Miners, whether individuals or businesses, must understand how their activities are taxed to avoid penalties and maximize their earnings.

In this blog, we have discussed in detail about the crypto mining taxes in 2025, covering everything from how mining works to deductions, IRS guidelines, and new tax proposals like the controversial 30% excise tax on mining operations.

So let us get started!

Crypto Mining’s Growing Relevance and Regulatory Attention

Cryptocurrency mining, the process by which new digital assets are created and transactions are verified on the blockchain, has evolved significantly since Bitcoin’s inception in 2009.

According to Statistica,

- The projected revenue in the cryptocurrency market is estimated to reach US$45.3bn worldwide by the end of 2025.

- It is also expected to demonstrate a compound annual growth rate (CAGR 2025-2025) of NaN%, resulting in a projected total of US$45.3bn this year.

The United States has become a dominant player in the mining industry, accounting for over 35% of Bitcoin’s global hash rate as of 2024. As mining operations scale and profitability increases, the IRS has heightened its scrutiny.

So, will Bitcoin mining be limited ONLY to the US?

What is Crypto Mining?

Crypto mining is the process of validating blockchain transactions by solving complex mathematical problems. Miners use specialized hardware, such as Application-Specific Integrated Circuits (ASICs) or high-performance GPUs, to perform these calculations. Successful miners are rewarded with cryptocurrency tokens, such as Bitcoin, or Ethereum, as an incentive for their efforts.

Crypto mining serves two primary purposes:

- Transaction Verification: Miners validate and secure transactions on the blockchain, ensuring data integrity and preventing double-spending.

- Token Creation: Mining introduces new coins into circulation, contributing to the overall supply of a cryptocurrency.

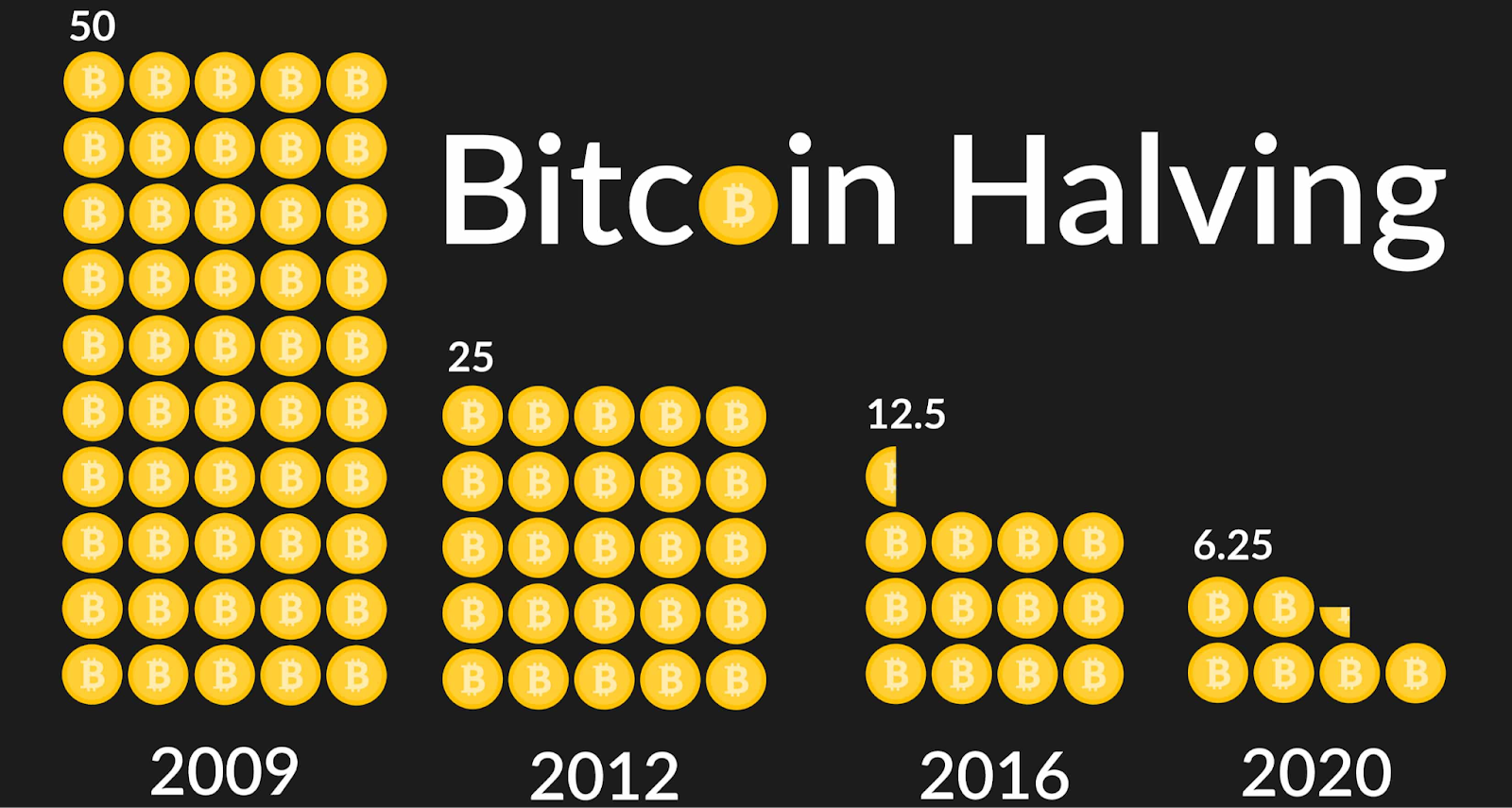

As of January 2025, Bitcoin miners receive 6.25 BTC per block mined (subject to halving events), while Ethereum validators earn staking rewards instead of mining rewards.

Crypto Mining Rewards

Mining rewards are the incentives you receive for successfully validating a block on the blockchain. These rewards consist of the following key components:

- Block Rewards: A fixed number of cryptocurrency tokens awarded to miners for successfully adding a new block to the blockchain.

- For Bitcoin: The current block reward is 6.25BTC per block

- For Ethereum: Validators earn staking rewards rather than traditional block rewards.

- Transaction Fees: Miners earn transaction fees from users who prioritize faster transaction confirmations. These fees vary based on network congestion and user demand.

For instance, during periods of high activity, such as market surges or significant events, the fees can constitute a substantial portion of miners’ income.

Did you know that you can gift crypto to reduce taxes:

Factors Influencing Mining Rewards

Crypto mining rewards are influenced by a variety of factors that can significantly affect the profitability and success of mining operations. Understanding these factors is important for miners aiming to optimize their earnings. Here are some of the key factors influencing mining rewards in cryptocurrency.

#1 Hash Rate and Mining Power

The hash rate is a critical measure of computational power and represents the number of calculations a miner can perform per second while attempting to solve cryptographic puzzles.

Miners with higher hash rates can solve blocks faster, increasing the chances of earning rewards.

For example, a mining rig with a hash rate of 100 TH/s can perform 100 trillion calculations every second, significantly enhancing the probability of successfully mining a block compared to a rig with only 10 TH/s.

On the other hand, when more miners join, the overall network hash rate increases, making it challenging for individual miners to earn rewards.

#2 Mining Difficulty

Mining difficulty adjusts approximately every two weeks based on the total computational power of the network.

If more miners join the network and the total hash rate increases, it becomes difficult to ensure that blocks are still mined every ten minutes. Conversely, if miners leave, the difficulty decreases.

Higher difficulty means it takes longer and requires more computational power to mine new blocks, deciding individual miners’ rewards unless they can keep up with technological advancements.

#3 Energy Consumption and Efficiency

Energy costs are one of the most significant expenses for miners.

Mining efficiency is often measured in joules per terahash (J/TH). Lower J/TH values indicate better energy efficiency. For instance, an efficient ASIC miner might operate at 30 J/TH, while older models could consume over 100 J/TH.

Miners located in regions with lower electricity costs have a competitive advantage. For example, areas with abundant renewable energy sources like hydroelectric power can offer significantly reduced rates compared to regions reliant on fossil fuels.

#4 Market Conditions and Bitcoin Price

The market price of Bitcoin directly influences mining profitability. Higher prices mean greater rewards for mined coins. Bitcoin undergoes halving approximately every four years, reducing block rewards by half (from 50 BTC in 2009 to 6.25 BTC in 2020 and 3.125 BTC in April 2024). This reduction impacts supply and can lead to price increases if demand remains strong.

#5 Regulatory Environment

The regulatory landscape surrounding cryptocurrency mining can significantly influence profitability.

Changes in tax laws or regulations can impose additional costs on miners. For instance, proposed taxes on energy consumption for mining could increase operational costs substantially.

Conversely, some regions may offer incentives for using renewable energy sources or for establishing mining operations that create jobs.

Read More: What do you need to mine cryptocurrency? Beginner’s Guide

How Is It Taxed? Does Crypto Mining Get Taxed?

Yes, cryptocurrency mining is taxable in the United States. The IRS treats mining rewards a taxable income, subject to specific rules depending on whether the activity is classified as a hobby or a business.

According to IRS, the taxable events related to cryptocurrency include:

- Sale of a digital asset for fiat

- Exchange of a digital asset for property, goods, or services

- Exchange or trade of one digital asset for another digital asset

- Receipt of a digital asset as payment for goods or services

- Receipt of a new digital asset as a result of a hard fork

- Receipt of a new digital asset as a result of mining or staking activities

- Receipt of a digital asset as a result of an airdrop

- Any other disposition of a financial interest in a digital asset

The following are not taxable events according to the IRS:

- Buying cryptocurrency with fiat money

- Donating cryptocurrency to a tax-exempt non-profit or charity

- Making a gift of cryptocurrency to a third party (subject to gifting exclusions)

- Transferring cryptocurrency between wallets

Taxation Process

Income Tax:

- When you mine cryptocurrency successfully, you must report its fair market value (FMV) as income on your tax return.

- FMV is determined by the price of the cryptocurrency at the time it was mined.

Capital Gains Tax:

- If you hold mined cryptocurrency and later sell it at a higher price than its FMV when mined, you'll owe capital gains tax on the profit.

- Short-term capital gains (for assets held less than a year) are taxed at ordinary income rates.

- Long-term capital gains (for assets held over a year) are taxed at lower rates (0%, 15%, or 20%, depending on your income bracket).

Is Bitcoin Mining Taxed Twice?

A common misconception is that Bitcoin mining is taxed twice. While mining rewards and subsequent transactions involving mined cryptocurrency are both taxable, they are taxed under different rules:

- Income Tax: When you mine Bitcoin or any other cryptocurrency, you pay income tax on its fair market value at the time you receive it.

- Capital Gain Tax: If you later sell or trade that cryptocurrency for a profit or loss compared to its original FMV when mined, you pay capital gain tax.

Although these are separate taxable events, they do not constitute "double taxation." Instead, they reflect the dual nature of mining rewards as both income and an asset.

Crypto Mining Tax Deductions

For miners classified as businesses, the IRS allows deductions for expenses directly related to mining activities. These deductions can significantly reduce taxable income.

Common Deductible Expenses

- Electricity Costs: Mining is energy-intensive, and electricity expenses are often the largest deduction for miners.

- Hardware Costs: The cost of mining rigs, GPUs, or ASICs can be deducted as a business expense.

- Depreciation: Mining equipment loses value over time. Miners can deduct depreciation under the Modified Accelerated Cost Recovery System (MACRS).

- Repairs and Maintenance: Costs for repairing and maintaining mining equipment are deductible.

- Internet and Hosting Fees: Expenses related to internet connectivity or data center hosting are eligible for deduction.

- Software and Security: Costs for mining software and cybersecurity measures can also be deducted.

What Happens If Crypto Mining Is Not Added to Income Taxes?

Failing to report crypto mining income can result in serious consequences, including penalties, interest, and even criminal charges in extreme cases. The IRS has increased its focus on cryptocurrency compliance, using advanced blockchain analytics tools to track unreported crypto activities. Here are the penalties for non-compliance:

Fines and Penalties:

- The IRS imposes penalties ranging from late filing fees to fraud penalties if income is intentionally omitted.

- Fines can reach up to $250,000 for severe non-compliance cases.

Interest Charges:

- Unpaid taxes accrue interest over time until fully paid.

Audits and Legal Action:

- The IRS uses advanced tools like blockchain analytics software (e.g., Chainalysis) to identify unreported crypto activity.

- Non-compliance could result in audits or even criminal charges in extreme cases.

Miners should prioritize accurate reporting and compliance with IRS guidelines to avoid these risks.

IRS Crypto Mining Guidelines

The IRS has been clear about how crypto mining activities should be reported:

- Mined cryptocurrency must be reported as ordinary income based on its fair market value at receipt.

- Hobbyist miners report income on Form 1040 Schedule 1; professional miners operating as businesses use Form 1040 Schedule C.

- Businesses may deduct expenses related to their operations; hobbyists cannot claim deductions beyond their earnings.

Increased enforcement measures by the IRS mean that miners must remain diligent about record-keeping and reporting all taxable events accurately.

The Proposed 30% Tax on Crypto Mining

In May 2023, the Biden administration proposed a Digital Asset Mining Energy (DAME) excise tax that would impose a 30% levy on electricity costs incurred by crypto miners in the U.S., citing environmental concerns over energy-intensive PoW mining operations.

Key Details:

- The proposed tax would apply incrementally over three years (10% in Year 1, increasing annually).

- It targets large-scale operations but could impact small-scale miners indirectly due to rising electricity costs.

- The DAME tax failed to be passed in 2023

Conclusion

Crypto mining in 2025 remains a lucrative but highly regulated activity. Miners face complex taxation rules, including income and capital gains taxes, while keeping an eye on potential changes like the proposed DAME excise tax. Here are some of the key takeaways:

- Report mined crypto as ordinary income based on its fair market value at receipt

- Maintain detailed records of all transactions and expenses

- Claim eligible deductions like equipment costs and electricity

- Follow IRS guidelines to avoid penalties and legal troubles

- Regulations are changing fast, so working with a tax professional who understands crypto can help you stay compliant and maximize your financial results

Need help navigating the crypto world? Learning Crypto offers expert guidance and comprehensive resources to tackle everything from mining to taxes. Let us simplify crypto for you!

Frequently Asked Questions

- How to avoid crypto taxes?

It is illegal to avoid paying taxes on crypto. So, it’s best to ensure you record all of your transaction dates, times, and amounts for accuracy. Otherwise, you risk an audit and being charged with tax evasion.

- Do You Pay Taxes on Cryptocurrency?

Yes. The type of taxes you pay and how much depends on the circumstances in which you acquired and used or sold your cryptocurrency, your income, and your tax status.

- Do You Have to Report Crypto Under $600?

If your gross income, including cryptocurrency, for a year was under the minimum filing requirements for your status, you're not required to file or report it. However, you may want to file, as you might be eligible for a refund. If your income exceeds the minimum filing requirements, you must report the crypto and any capital gains and losses.

:max_bytes(150000):strip_icc()/GettyImages-929584582-9d7790de3ee44f658a9580cc598c641f.jpg?ref=learningcrypto.com){kind=link}

{kind=link}